Rollover an existing IRA

Unlike with employer-sponsored retirement plans such as 401k’s, 401a’s, 403b’s and 457’s where the money is in the employers name your merely a participant not an owner meaning your employer can change plans without your approval, they determine the investment selections or limit your plan’s investment options without your say-so, there is usually a vesting schedule on the employer money if they even offer you a matching plan and they can automatically enroll you into the plan and even force an involuntary payout without your discretion ( Safe Harbor). Fees and costs are higher 👆 and leaving your job means losing your ability to further contribute to the retirement plan. Inactive accounts often go unmanaged, underperform or sit in cash. An Individual Retirement Account (IRA) allows you to put the money in your name it’s your own account 🫵 you do not have to play by their rules and you can select your own investments from a much larger pool of options. Your access is unchanged and you can still contribute even if you decide to switch jobs and you can even rollover that old 401k, 401a, 403b or 457 retirement plan and consolidate it into an IRA where the fees and costs are lower 👇 or into a fixed indexed annuity. At Khatter Financial 🦚 we specialize in working with clients and businesses who have been contributing to their employer-sponsored retirement plans while helping them reduce their current years taxable income and getting them a rate of return on money they would have had to otherwise pay in tax. We would love to have a conversation with you about how we can add value to your portfolio.

Individual Retirement Arrangements (IRAs) | Internal Revenue Service (irs.gov) = The IRA contribution limits for 2026 are $7,500 for those under age 50, and $8,600 for those age 50 or older. Depending on your situation, you may be eligible to make contributions to an IRA and receive either tax-deferred or tax-free distributions. You have until April 15, 2027 to make a contribution for tax year 2026. Please submit ahead of time to allow a few days for processing do not wait until the last minute. Contact us and we can objectively consider which options may be best for your retirement goals.

https://www.voya.com/tool/inherited-ira-rmd-calculator= Inherited IRA RMD calculator. Contact us for assistance.

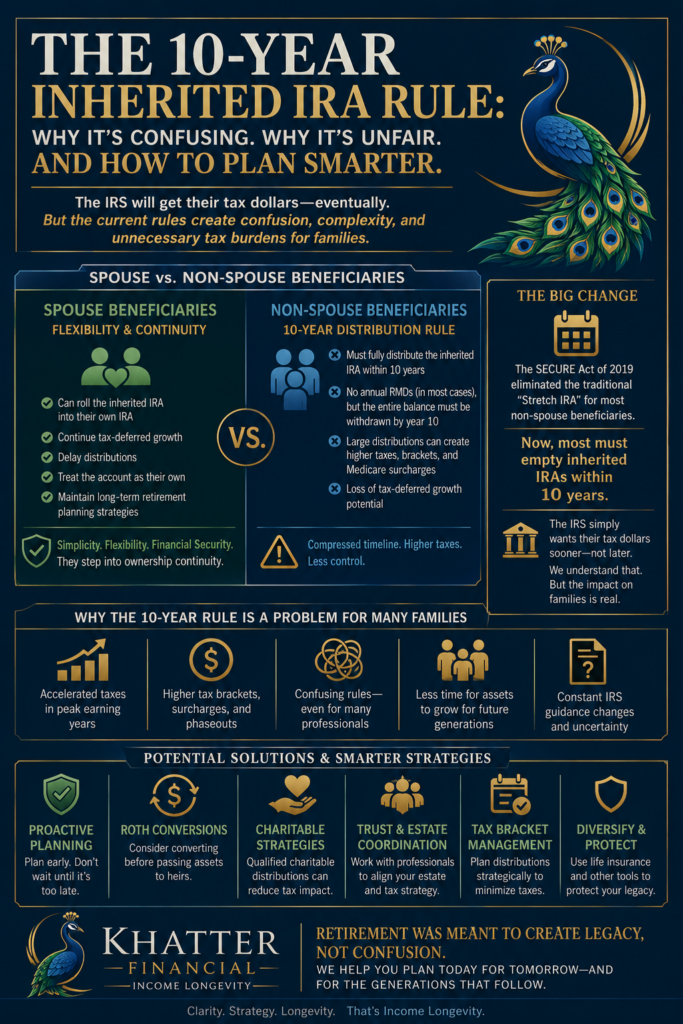

(1) The 10-Year Inherited IRA Rule: Why Many Families Feel the System Became Needlessly Complicated | LinkedIn = Read the article.

Retirement topics – Beneficiary | Internal Revenue Service (irs.gov) = SECURE Act Changes

Roth acct in your retirement plan | Internal Revenue Service (irs.gov) = Earnings are tax-free after 5 years and over 59 1/2. There is no required minimum distribution. Contact us for assistance.

sep-retirement-plans-for-small-businesses.pdf (dol.gov) = A self-employed business owner can contribute up to the lesser of $72,000 or 25% of compensation for 2026. Contact us about how a SEP IRA can be a good option for your business.

Avoid the #1 Inherited IRA Mistake

What a Better Strategy May Help You Do

Your Suggested Next Step

Request Your Personalized Inherited IRA Strategy

Many business owners are not taking full advantage of this.

Build My SEP IRA Strategy

A SEP IRA could allow you to reduce taxable income while building long-term retirement savings. The next step is to review how this fits into your overall retirement, tax-deferral, and income strategy.

Request Your Personalized SEP IRA Strategy